The Amenity Premium: How Walkable Neighbourhoods Are Quietly Rewriting Britain's Property Value Hierarchy

Photo: Tom Jolliffe , CC BY-SA 2.0, via Wikimedia Commons

The Amenity Premium: How Walkable Neighbourhoods Are Quietly Rewriting Britain's Property Value Hierarchy

There is a particular quality to a neighbourhood that works on foot. The independent baker whose queue spills onto the pavement on a Saturday morning. The primary school whose gates anchor the rhythm of the surrounding streets. The small park where, on a dry Tuesday afternoon, someone is always walking a dog. These are not luxuries — they are the functional infrastructure of daily life — and Britain's property market is, with increasing clarity, pricing them accordingly.

For much of the post-war period, the dominant narrative of residential value was one of connectivity to employment. The arrival of a new rail station, the extension of a motorway junction, the opening of a tram line — these were the events that property investors tracked, confident that transport infrastructure would reliably translate into price appreciation. That relationship has not disappeared. But alongside it, and in some markets ahead of it, a new variable has asserted itself with considerable force: the walkability of the immediate environment.

What the Data Is Telling Us

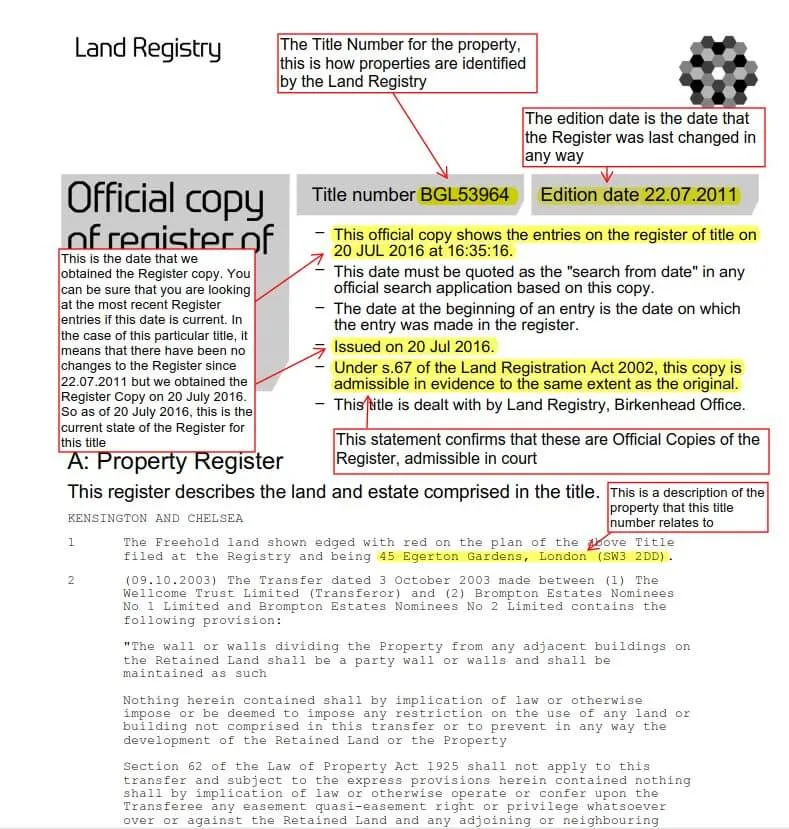

The evidence base for what practitioners are increasingly calling the 'amenity premium' has strengthened considerably in recent years. Analysis of Land Registry transaction data, cross-referenced with walkability indices and local amenity mapping, consistently identifies a material price differential between properties within comfortable walking distance of everyday services and those that require a car journey to access equivalent provision.

Photo: Land Registry, via landregistry-deeds.co.uk

Photo: Land Registry, via landregistry-deeds.co.uk

The premium varies by market and by the specific amenity in question, but the broad pattern is consistent. Properties within a ten-minute walk of a good primary school command measurable uplift over comparable stock that falls outside the catchment boundary. Access to quality green space — not the distant municipal park, but the usable, attractive space within a short walk — adds further value. And increasingly, the presence of independent food and beverage operators — the café, the deli, the farmers' market — functions as a leading indicator of neighbourhood desirability that buyers are actively seeking out and paying for.

What has changed in the post-pandemic period is the relative weighting of these factors. Research conducted across multiple British housing markets suggests that walkability metrics have risen in buyer priority rankings at the direct expense of commute time. For a significant proportion of the workforce now operating on hybrid patterns — in the office two or three days a week rather than five — the character of the neighbourhood in which they spend the majority of their time has become a more pressing consideration than the speed of the journey they make less frequently.

The Developer's Calculus

For the development industry, this shift in buyer and renter behaviour carries direct implications for how schemes are conceived, designed, and brought to market. The traditional approach — deliver the residential units, assume that amenity will follow as the neighbourhood matures — is increasingly being challenged by evidence that amenity provision at the outset, or secured through planning obligations, produces measurably better sales values and absorption rates than schemes that leave residents to wait for the market to respond.

Forward-thinking developers are approaching this challenge from several directions simultaneously. At the design stage, the integration of active ground-floor uses — commercial units sized and priced for independent operators rather than national multiples — creates the conditions for the kind of characterful local offer that buyers are seeking. The difference between a ground-floor unit designed for a chain coffee operator and one designed to attract an independent baker is not merely aesthetic; it reflects a deliberate strategic choice about the kind of neighbourhood the developer intends to create and the premium they expect to achieve as a result.

At the planning stage, the Section 106 process — long viewed primarily as a mechanism for extracting affordable housing and infrastructure contributions from developers — offers an underutilised tool for securing community amenity. Obligations that lock in the provision of healthcare facilities, nurseries, or community spaces within new developments serve both the planning authority's objectives and the developer's interest in establishing walkable amenity from day one of occupation.

Engineering Walkability from the Ground Up

The concept of walkability extends beyond the presence of amenities to encompass the physical design of the streets and spaces that connect them. A development that places a café within 200 metres of every front door but routes pedestrians through car-dominated service roads and underlit subways has not genuinely delivered walkability — it has delivered proximity whilst undermining the experience that makes proximity valuable.

Urban designers working on contemporary British residential schemes are increasingly drawing on established frameworks — most notably Walk Score methodologies adapted for UK contexts and the '15-minute neighbourhood' principles that have gained significant traction in planning policy discussion — to audit and optimise the pedestrian experience within proposed developments. Street widths, crossing provision, lighting, planting, and the active or passive frontages that line a route all contribute to whether residents choose to walk or default to the car.

Photo: Walk Score, via blogger.googleusercontent.com

Photo: Walk Score, via blogger.googleusercontent.com

The distinction matters financially as well as philosophically. Schemes that score well against walkability criteria on independent assessment are demonstrating a capacity to command and sustain price premiums that less walkable contemporaries cannot match. For build-to-rent operators — for whom the long-term rental income profile of a scheme is the primary value driver — the retention benefits of a genuinely walkable neighbourhood are equally significant. Residents who feel well-served by their immediate environment renew their tenancies at higher rates, reducing the void and re-letting costs that erode net operating income.

The Independent Operator Effect

One of the more nuanced findings to emerge from amenity research is the disproportionate value attributed by buyers to independent, locally owned businesses compared with national chain provision of equivalent function. Two postcodes may each offer a café, a pharmacy, and a convenience store within walking distance — but if one neighbourhood's offer is composed of independent operators and the other of national multiples, the former will typically command the higher premium.

This preference reflects something deeper than aesthetic taste. Independent operators signal neighbourhood confidence — they are entrepreneurs who have made a personal financial commitment to the success of a specific location. Their presence suggests that the neighbourhood has reached a point of viability that attracts genuine investment, rather than the formulaic roll-out of a brand's site acquisition strategy. For developers, the implication is that the terms on which ground-floor commercial space is offered — rents, lease lengths, and the restrictions placed on use — directly influence the type of operator attracted, and therefore the value generated for the residential units above.

A Structural Shift, Not a Passing Trend

It would be tempting to characterise the amenity premium as a post-pandemic phenomenon that will moderate as working patterns settle and commuting reasserts its primacy. The evidence does not support this interpretation. The preference for walkable, amenity-rich environments predates the pandemic, is rooted in demographic trends — particularly the growth of older owner-occupier and renter populations for whom car dependency is a practical concern — and is reinforced by an environmental consciousness that is influencing purchasing decisions across age groups.

For HMS Developments, and for the broader development industry, the strategic conclusion is straightforward. Amenity is infrastructure. It requires the same deliberate investment, the same early-stage planning, and the same long-term thinking that developers routinely apply to roads, drainage, and utilities. Schemes that treat it as an afterthought will find themselves competing at a disadvantage against those that have understood, and responded to, one of the most consequential shifts in British residential market behaviour in a generation.